Most people assume that identifying the controller of a company is a straightforward exercise in reading a shareholder table. In reality, modern corporate governance is less like a clear ledger and more like a set of “corporate nesting dolls,” where one entity hides another, which in turn hides another. The stakes of understanding these structures are high. For AML officers, the inability to see who is truly pulling the strings is not just a technical failure—it is a massive real-world risk. Relying on simple thresholds of 25% or 50% ownership often creates an illusion that masks the actual distribution of power. To achieve clarity, we must move beyond simple percentages and embrace the technical precision of Integrated Ownership and Voting Power.

Here are five surprising truths about the reality of global corporate ownership.

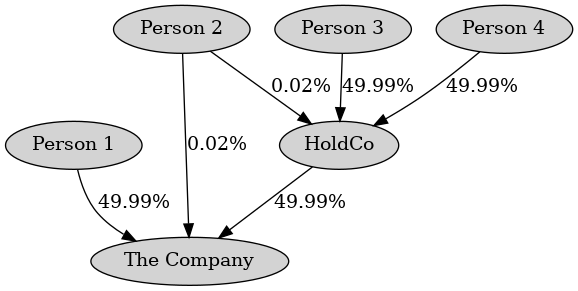

1. You Can Be Highly Powerful With Just 0.03% Ownership

It is a common misconception that influence is directly proportional to the amount of money a person has invested. In complex structures—frequently seen in generational family companies—cross-shareholdings can decouple “cash rights” (the right to profits) from “voting power” (the right to make decisions). In one real-world scenario, a specific individual (Person 2 in the figure) was found to be the most powerful actor in a company despite having an integrated ownership stake of just 0.03%.

This individual held small, direct votes and by aligning these different paths of control, Person 2 possesses a level of influence far exceeding their microscopic financial stake. Share of voting rights is not a suitable measure for the level of influence a shareholder has in the company.

This gap between ownership and influence means that traditional AML checks focusing only on high-percentage shareholders potentially miss powerful actors in a network.

2. The “Family Factor” and the 13-to-1 Discrepancy

Even when data is available, different legal frameworks can produce — very confusingly — different results for the same company. Analysis of the Norwegian Beneficial Owners (RRH) register reveals a significant “regulatory blind spot” created by the discrepancy between register legislation and AML legislation. Under the Norwegian Register of Beneficial Owners Act, a company—like Berge BA in the example—might list only one beneficial owner. This is because the register law uses a strict 50% control threshold to move down the ownership chain.

However, under the more stringent AML legislation (§14), which uses a lower threshold (>25%) at every step, that same company—Berge BA—is calculated to have 13 beneficial owners. The primary driver of this jump from 1 to 13 beneficial owners is the “Family Factor.” AML law requires that close family relations be treated as a single unit when considering beneficial ownership, whereas the register law contains no such provision.

Register Law View: One person identified based on a 50% control threshold.

AML Law View (§14): Thirteen people identified due to a 25% threshold and the mandatory grouping of family units. For banks and reporting entities, this inconsistency means that noncritical trust in an official government register can lead to a failure to meet statutory AML obligations.

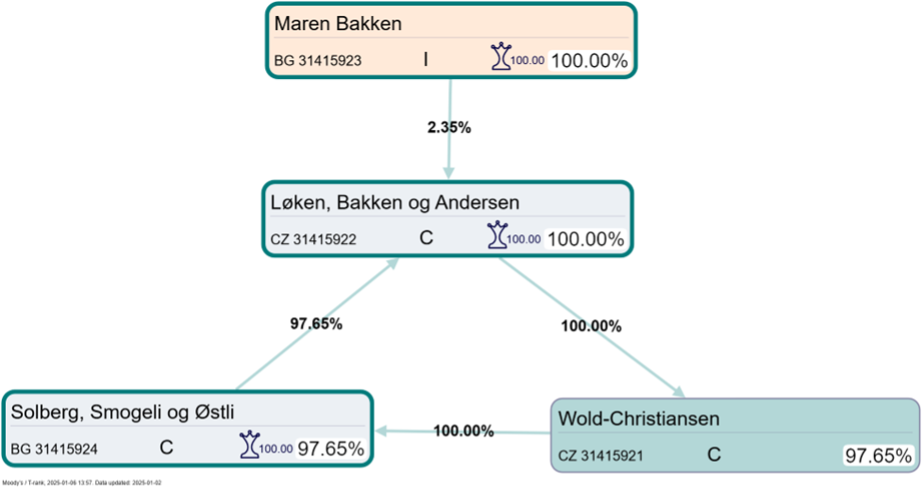

3. The Circular Loophole: Where Companies Own Themselves

Circular ownership occurs when a chain of companies eventually loops back to the start—for example, Company A owns Company B, which owns Company C, which in turn owns a stake in Company A. This creates a phenomenon of self-ownership that renders traditional bottom-up analysis useless. In a study of a Czech company, a single individual held a direct ownership stake of only 2.35%. Under standard analysis, this person would never be flagged as a controller. However, because the company indirectly owned 97.65% of itself through a circular ownership structure, that 2.35% stake effectively translated into 100% control of all outstanding votes.

Circular ownership creates a difference between direct ownership and the integrated/indirect ownership, and this discrepancy makes it hard to understand who is actually a Beneficial Owner.

This is a global phenomenon; in Japan and South Korea, circular ownership structures even have their own terms and are known as Keiretsu and Chaebols, respectively. These structures provide stable financing and mutual assistance but profoundly obscure transparency. Significant circular ownership is found in territories worldwide, with the Russian Federation, Germany, and Norway appearing in the top 10 list of regions where these obfuscating structures are most prevalent.

4. Why “50% Ownership” Fails

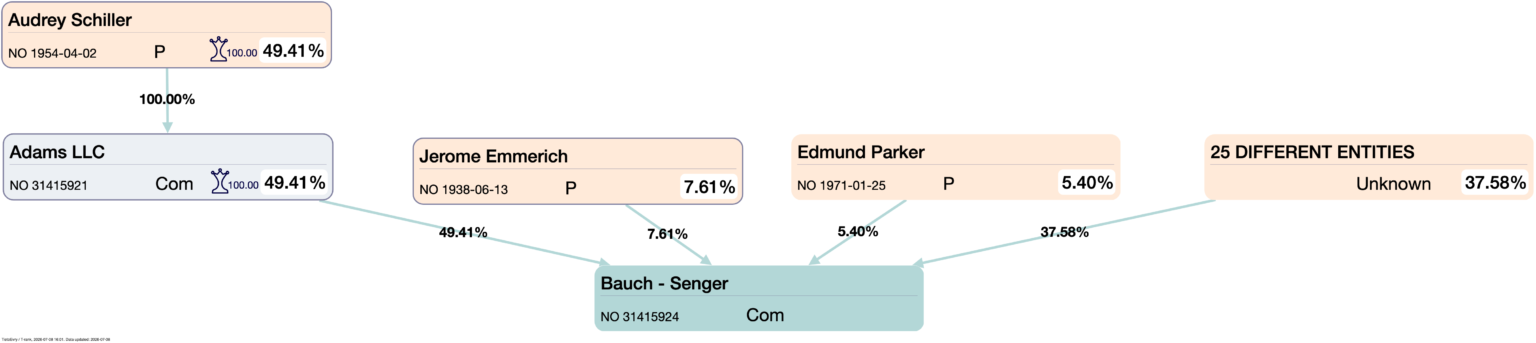

The financial world often uses the Threshold Model: if you own 50% plus one share, you are in control. If you own less, you are not. This all-or-nothing approach lacks the nuance required for modern, dispersed ownership networks. Using the Voting Power (Banzhaf Power Index), we can measure de Facto Control. This model calculates the probability that a voter will be “pivotal” (the swing voter) across all possible random voting scenarios.

Consider an owner like Audrey Schiller in the above example, who holds a 49.41% stake in the company of interest. The Threshold Model says she is not in control. However, if the remaining 50.59% is spread across dozens of small shareholders, the Voting Power math shows that Audrey Schiller is the pivotal voter in 99.9999% of all potential voting combinations.

Why the Threshold Model Fails:

– Ignores Dispersion: The Threshold Model fails to account for whether the remaining 51% is held by one consolidated block or 500 independent actors.

– Underestimates Swing Power: A 20% owner can be a “kingmaker” if other owners are split.

– Missing De Facto Reality: The Threshold Model treats power as a binary switch rather than a statistical likelihood of dominance in random voting coalitions.

5. Official Registers are “Works in Progress,” Not Ground Truth

While official national registers are a step toward transparency, they are not yet a gold standard. An analysis of the Norwegian register as of August 2025 found that 14%-16% of entities had significant deviations from independent data sources when using the register’s own definition. More alarmingly, when the AML law definition (§14) was applied to the same register, the compliance rate dropped to 78%. This means there is a 22% deviation between what the law requires a bank to know, and what the government register actually provides. These deviations fall into two main categories:

– Illegitimate Deviations: Intentional obfuscation to hide control structures, or simple negligence by owners who find beneficial ownership definitions too complex to navigate.

– Legitimate Deviations: Outdated independent data (such as tax records from the previous year) or the existence of private shareholder agreements that are legally reflected in the register but not in public records.

The Future of Transparency

The landscape of corporate transparency is shifting from a manual and theoretical exercise to a high-tech discipline powered by automated network analysis. The upcoming EU Anti-Money Laundering Regulation (AMLR), set to apply from July 2027, aims to harmonize these rules across the continent. However, the AMLR introduces potential new problems. While it mandates Integrated Ownership calculations, it introduces a dangerous logical inconsistency in Article 52 by attempting to mix voting rights into the mathematical calculation of ownership interest. Experts warn that mixing these two distinct concepts could lead to additional confusion for compliance officers.

In an age of skyrocketing digital data, we can no longer afford to look at ownership as a simple list of names. To truly understand who owns the companies in the world, we must stop looking only at the nodes and start looking at the network.

The critical question remains: Is your organization still looking at a list, or are you finally seeing the network?

Written by Kenth Engø-Monsen – kenth (at) trank (dot) no